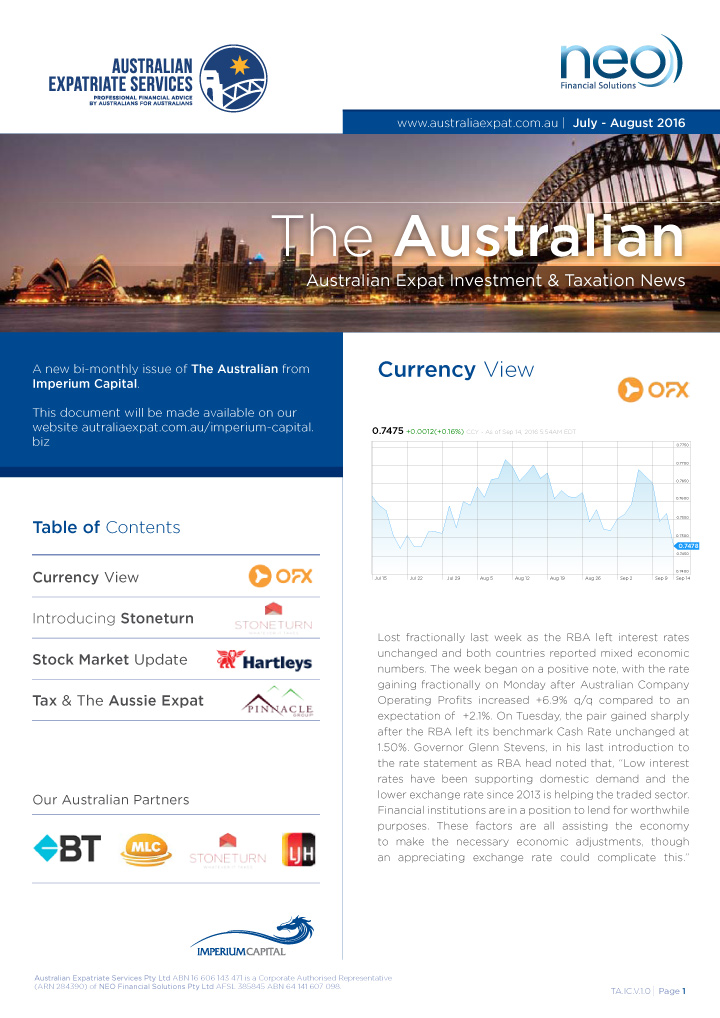

Currency View by OFX

Last week’s news

- Joe Biden pleaded for US Congress to ‘act now’ on a new $1.9tn economic rescue plan, setting it up as his top legislative priority as he prepares to enter the White House this week. The plan includes new direct payments to Americans, aid for state and local governments and more funding for the coronavirus pandemic response. The health of the US economy was thrown back into the light last week after an unexpected jump in first-time weekly claims for jobless benefits and consumer sentiment weakening more than expected in January.

- The UK economy shrank for the first time in six months in November and risks entering a double-dip recession even though the latest contraction was less severe than expected. UK output fell 2.6% compared to October, the first contraction since April 2020’s lockdown. The figure was however better than the 5.7% contraction expected, and some economists suggested the UK has now built some immunity to lockdowns; UBS head economist Dean Turner stated that ‘households are better prepared for the current restrictions, which means that any economic weakness is likely to be significantly less’.

- Donald Trump became the first President in US history to be impeached for a second time as the House of Representatives charged him with ‘incitement to insurrection’ for his role in stirring up a mob of supporters that stormed the Capitol last week. The House voted 232 to 197 last Wednesday in favour of impeaching the President after the riot that left five people dead, with 10 Republicans breaking ranks to support all Democrats in voting to charge Mr Trump. Nancy Pelosi, the house speaker added that ‘Donald Trump is a clear and present danger to our country’. A Consult poll published last Wednesday showed Mr Trump’s approval rating had dived to an all-time low, with just 34% of voters approving of the job he was doing.

- An exit from easing conditions in G7 countries seems difficult now. Capital markets, especially FX markets, are operating today with high confidence that the Fed has no alternative but to maintain highly favourable conditions, i.e. short-term near zero interest rates, massive ongoing balance sheet growth, and whatever it takes to maintain market liquidity. For now, the huge pile of cash might limit the upside in treasury yields in the US and in the world. However, anticipation of what a Democratic government means has jump-started inflation expectations in the US, pushing long-term treasury yields back to the highs seen in March 2020.

- The pandemic is escalating in the US and Europe, and the economic situation might be more evident in the coming months. Active COVID-19 cases in Germany almost tripled in the past month. In France, cases have doubled, and in the US, they have increased by 50%. Governments around the world have enacted partial lockdowns, nonetheless, it is not unreasonable to fear a further spike in cases over the next month or so at a time when health systems are already stressed.

Looking ahead

- There is news that front-runner Friedrich Merz, a wealthy corporate lawyer who has been involved in German politics for more than three decades, might be elected as leader of Germany’s Christian Democratic Union party to replace Angela Merkel. Merz is seen as a conservative candidate who wants to shift directions to the right and has been critical of the EU and ECB in the past.

- Despite the strength of the US dollar last week, the British pound was the best performer, increasing 0.16% against the US dollar. The pound also increased 2%, 1.3%, 0.9% and 0.4% versus the Swedish krona, euro, Aussie dollar, and loonie. In line with the moves, leveraged funds raised their net-bullish position on the pound to the highest level since October, according to data from the Commodity Futures Trading Commission for the week through January 12th. They also increased euro longs to the most since late December.

Key market events this week

- Wednesday

- GBP Core Inflation Rate YoY (Dec)

- EUR Core Inflation Rate YoY (Dec)

- CAD Core Inflation Rate YoY (Dec)

- Bank of Canada Interest Rate Decision

- AUD Westpac Consumer Confidence Index (Jan)

- Thursday

- AUD Employment Change & Unemployment Rate (Dec)

- Bank of Japan Interest Rate Decision

- ECB Interest Rate Decision and Press Conference

- NZD Inflation Rate YoY (Q4)

- JPY Inflation Rate YoY (Dec)

- Friday

- USD Markit Manufacturing PMI (Jan)

Disclaimer

Note that specialist Accounting, Property, Mortgage and Foreign exchange services offered by our partners, Stoneturn, OFX, Hartley’s and LJ Hooker are via referral arrangement only. Australian Expatriate Services are not responsible for any advice/services provided by these Firms.

{kind=link}